How Prop Firms Make Money: The 90% Failure Rate & Hidden Rules Explained

From evaluation fees to B-book execution: an honest look behind the scenes of the modern prop firm business model.

There's a widespread saying in retail trading: "During a gold rush, sell shovels." When it comes to proprietary trading firms, this adage rings louder than ever. While many firms do indeed profit when their long-term funded traders succeed, the staggering truth is that the business model relies heavily on the fact that the vast majority of traders will fail.

Understanding exactly how prop firms make money is crucial for any aspiring funded trader—especially for retirees who need to treat their trading capital with absolute respect. By knowing where the firm's incentives lie, you can better navigate the evaluation rules and give yourself a mathematical edge.

The Truth in the Numbers: Real Prop Firm Statistics

While specific data varies slightly by firm and market conditions, industry-wide analysis and public data releases over recent years reveal a consistent, mathematically strict funnel:

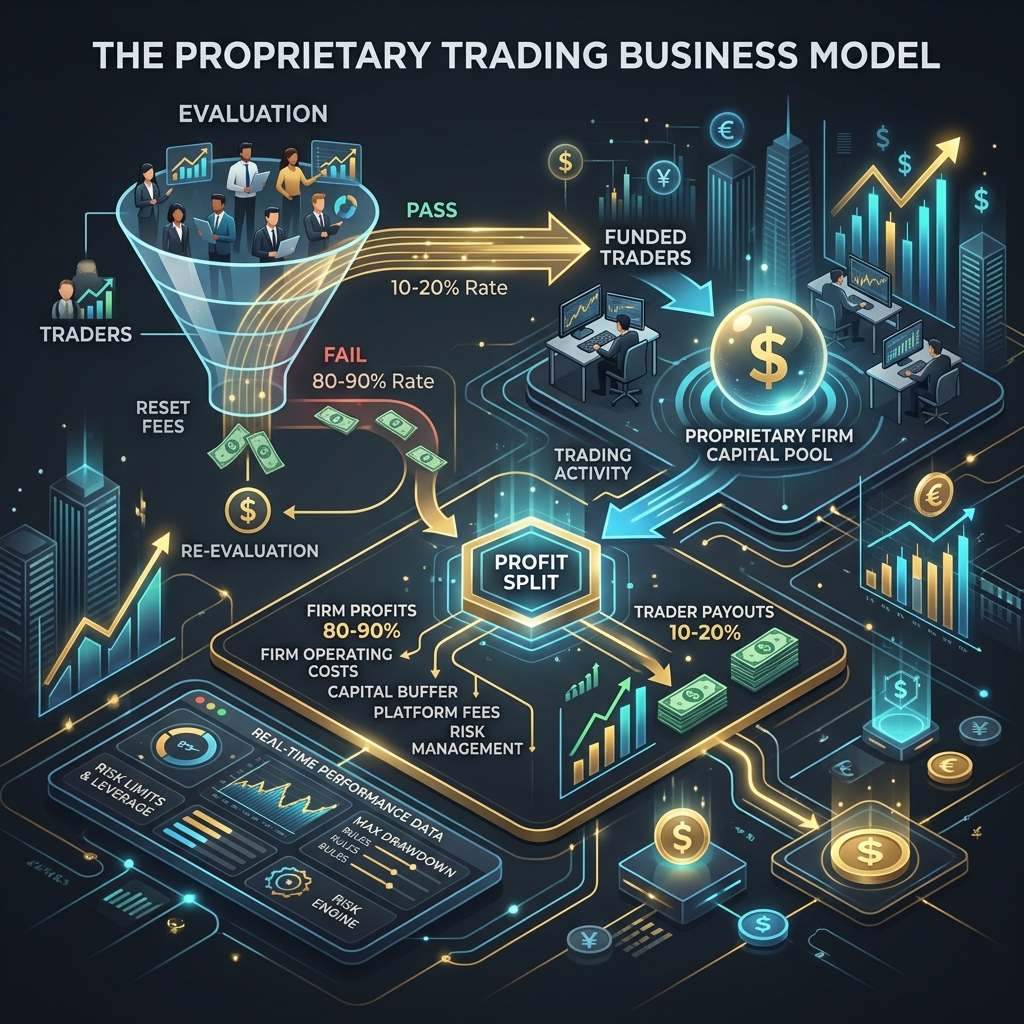

- Evaluation Pass Rate (5% - 10%): Less than one in ten traders successfully passes a Phase 1 or 1-Step evaluation on their first attempt.

- Funded Account Failure Rate (80% - 90%): Passing the challenge is only half the battle. Among those who receive a funded account, a massive majority lose that account within the first few months due to breaking drawdown rules or over-leveraging.

- Long-Term Payout Rate (~7%): Studies from major review sites indicate that only around 7% of all traders who originally purchase an evaluation will ever see a successful payout.

- Active, Long-Term Success (<1% - 2%): Over a 1-year timeline, a negligible fraction of traders successfully transition into long-term, professional income earners.

Revenue Breakdown: Evaluation Fees vs. Trading Profit

Where exactly does the revenue come from? The modern online "prop firm" space (which often involves simulated funding) operates differently from traditional Wall Street proprietary trading desks.

1. Evaluation and Challenge Fees (80% - 90% of Revenue)

The lifeblood of most retail prop firms is the recurring revenue generated by evaluation fees, reset fees, and monthly platform subscriptions. Because 90% to 95% of traders fail, these collected fees form a massive pool of capital.

In an ideal, sustainable business model, this capital pool is used to:

- Cover overhead, marketing, and operational costs.

- Provide a buffer to pay out the 5% to 10% of traders who successfully become consistently profitable.

2. Real Market Trading Profits (A-Booking) vs. Simulation (B-Booking)

Once you become funded, how does the firm make money on your trades? This introduces the concept of A-Book vs. B-Book execution.

A-Book (Copying Trades to the Live Market)

When a trader proves they are consistently profitable, a legitimate firm will copy their trades into a live, real-money brokerage account. The firm keeps around 10% to 20% of your profits, actually making money with you in the real market.

B-Book (Keeping You on Simulation)

Because most funded traders still blow their accounts (the 80-90% failure rate mentioned earlier), many firms keep funded traders on a high-quality simulated environment. When you request a payout, the firm pays you out of their internal pool of evaluation fees, essentially acting as the counterparty to your risk.

The Hidden Rules Designed to Manage Risk (And Stop You Out)

Proprietary firms use extremely strict risk management protocols. While they protect the firm from ruin, these rules are notoriously difficult for beginners to navigate and contribute heavily to the high failure rate.

- Intraday Trailing Drawdowns: Some of the hardest rules to navigate. Instead of calculating drawdown at the end of the day, it is calculated from your highest open profit. If a trade goes $1,000 in your favor and you don't take profit, and it returns to breakeven, you just lost $1,000 of your allowed drawdown.

- Minimum Trading Days vs. High Frequency: Firms often require minimum trading days to prevent lucky "all-in" gambles, but some also ban High-Frequency Trading (HFT) and micro-scalping because it exploits simulated execution environments.

- Consistency Rules: To ensure you didn't pass through a single lucky news event, firms often dictate that no single trading day can account for more than 30% of your total profits.

- News Trading Restrictions: Volatility during CPI or FOMC events is erratic. B-Book firms hate extreme news events because simulated pricing and slippage differ from live market conditions, so they simply ban holding positions during those windows.

Why Some Prop Firms Have Longevity While Others Fail

The sudden explosion in prop firm popularity in recent years has led to both massive success stories and spectacular company collapses. So why do some firms thrive while others declare bankruptcy?

Firms that fail generally operate structurally like a Ponzi scheme—they rely entirely on new challenge sign-ups to pay their successful funded traders. If marketing slows down and the influx of new evaluation fees drops, they suddenly don't have the cash to pay their profitable B-book traders.

Conversely, firms with longevity use exceptional data modeling. They identify the top 1% of traders and reliably copy their trades to live markets (A-Booking), using real market profits to fund their operations. They don't just rely on challenge fees; they actually utilize their talented trader pool as an asset.

The Bottom Line for Traders

Understanding that 90% of a firm’s evaluation revenue comes from failed traders shouldn't discourage you. Instead, it should serve as a stark warning: You must treat risk management with surgical precision.

The prop firm model works beautifully for the patient, disciplined trader. By understanding exactly how and why firms lay out their rules—to filter out impulsive gamblers and identify consistent risk managers—you can align your strategy to ensure you fall on the profitable side of the statistics.

Brendan Nolan

Retired Trader & Founder

After spending 25+ years as a Product Management executive designing platforms for the nation's top 401(k) and retirement providers, Brendan transitioned into active futures trading in his 60s. He built PropFirmRetiree to help late-career professionals apply disciplined, risk-first principles to prop firm trading.

Read Brendan's Story →